Let's work together to unlock your financial potential and achieve your dreams

Learn More About Life Insurance

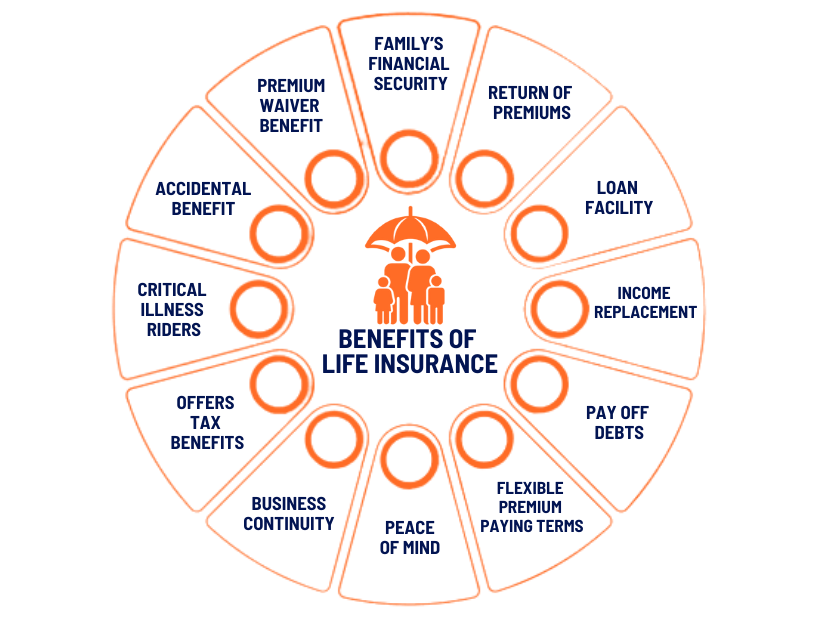

Life insurance is a financial contract between an individual and an insurance company, wherein the individual (policyholder) pays regular premiums in exchange for a promise that the insurance company will provide a lump sum payment or periodic payments to designated beneficiaries upon the policyholder's death. This payment is intended to offer financial protection and support to the policyholder's loved ones or dependents in the event of their passing. The primary purpose of life insurance is to provide financial security and help mitigate the potential economic impact that may arise due to the loss of the policyholder's income or financial contributions.

Term Life Insurance : It is the most basic and affordable form of life insurance in India. It provides coverage for a specified term & pays out a death benefit to the nominee if the insured person passes away during the term.

Whole Life Insurance : It is a type of permanent life insurance that provides coverage for the insured person's entire lifetime and includes a cash value component that grows over time.

Return of Premium (ROP) : It is a type of term life insurance policy that refunds the total premiums paid by the policyholder at the end of the policy term if the insured person survives the term.

Joint Life Insurance : It is a type of policy that covers two or more individuals under a single insurance contract, with the death benefit paid out upon the first insured person's demise. It is often chosen by couples or business partners to provide financial protection in case of one person's death. Joint life insurance can be more cost-effective than purchasing separate policies for each individual.

Endowment Plans : Endowment policies combine life insurance coverage with savings and investment components. They offer both a death benefit and a maturity benefit, which is paid out if the insured survives the policy term. Endowment plans are often used for long-term financial goals like education or retirement planning.

Unit-Linked Insurance Plans (ULIPs) : ULIP’s are investment-cum-insurance products that allow policyholders to invest in a variety of funds (equity, debt, or hybrid) while also providing life insurance coverage. A portion of the premium goes toward insurance, and the remaining amount is invested in the chosen funds. ULIP’s offer flexibility in fund selection and premium payments.

Money-Back Policies : They are similar to endowment plans but provide periodic payouts during the policy term. Policyholders receive a percentage of the sum assured at regular intervals, which can be useful for meeting various financial milestones.

Child Plans : They are designed to secure a child's future by providing funds for their education, marriage, and other needs. These policies typically have a maturity date that coincides with the child's future financial requirements.

Pension Plans/Annuity Plans : They are aimed at providing a regular income stream to policyholders after retirement. Policyholders invest a lump sum or make periodic contributions during their working years and receive a steady income during retirement.

Group Life Insurance : Group life insurance is often provided by employers as part of their employee benefits package. It covers a group of individuals under a single policy, offering cost-effective coverage.

Disclaimer : It is important to carefully review and understand the terms and conditions provided by the insurance company. The information provided should not be taken as financial advice, and it's recommended to consult with a qualified financial advisor to ensure that the policy aligns with your specific financial goals and needs. Policyholders should assess their coverage requirements, the suitability of the policy term, the accuracy of information provided during the application, and any associated premium payments. Additionally, potential policyholders should be aware that the benefits and payouts are subject to the terms outlined in the policy documents, and any discrepancies or questions should be clarified with the insurance company.